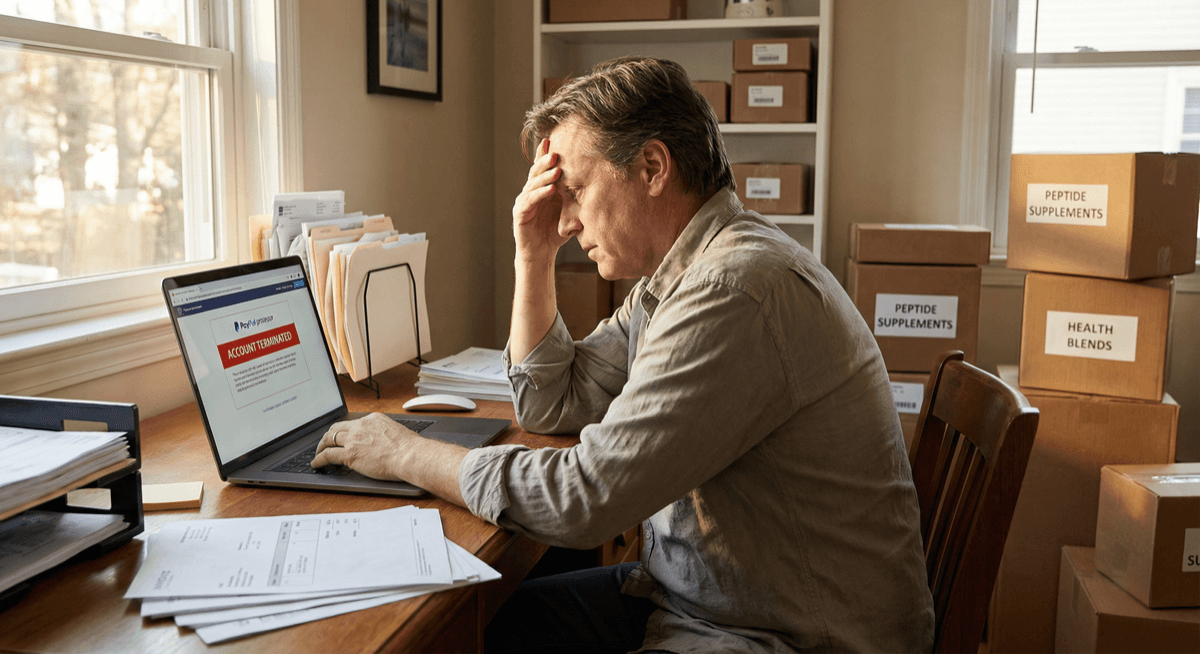

If your peptide merchant account was terminated, you're likely dealing with:

- Declining transactions that were previously working

- Frozen or delayed funds still held by your processor

- Customer checkout failures costing you sales in real time

- Advertising campaigns still running with nowhere to convert

- Urgency to restore processing before revenue loss compounds

First, take a breath. Termination does not mean your business is over — but your next steps matter significantly. The difference between a fast recovery and a drawn-out struggle comes down to how methodically you approach the process.

This guide explains what causes peptide merchant account terminations, what to do immediately, and how to secure stable processing again.

Step 1: Identify Why the Account Was Terminated

Merchant accounts are typically terminated for specific risk triggers, not random reasons. Understanding exactly what happened prevents you from repeating the same mistake with your next provider.

Common causes include:

- Excessive chargebacks — your dispute ratio exceeded Visa's 0.9% or Mastercard's 1.0% threshold

- Fraud spikes — unauthorized transactions slipped through weak filters

- Processing outside approved parameters — volume or ticket sizes exceeded what underwriting approved

- Compliance or website issues — product language, missing policies, or misleading claims

- Sudden volume increases — growth that looked like fraud to monitoring systems

- Reserve or monitoring violations — failure to meet conditions set during underwriting

Your termination notice or final communication from the processor should include or reference the reason. If it's unclear, ask for specifics — you need this information for your next application.

For a deeper breakdown of why shutdowns happen: Why Payment Processors Shut Down Peptide Businesses.

Step 2: Determine If You Were Placed on MATCH

After termination, you may be added to the MATCH list (Member Alert to Control High-Risk Merchants). This is a database managed by Mastercard that acquiring banks check when reviewing new merchant applications.

If you were placed on MATCH:

- The listing remains active for five years

- Future applications undergo stricter scrutiny

- Some processors will decline automatically

- You'll likely need to work with a high-risk specialist

Not all terminations result in MATCH placement, but chargebacks (reason code 04) and fraud (reason code 05) almost always do.

Learn how MATCH works and what it means for your next application: MATCH List for Peptide Merchants.

Being on MATCH does not make approval impossible — but it does require a more structured, high-risk underwriting pathway with a provider experienced in these situations.

Step 3: Stabilize Your Website and Policies

Before applying with a new processor, fix any gaps that may have contributed to the termination — or that could cause the same problem again.

- Review refund and shipping policies — ensure they're clear, visible, and realistic

- Check billing descriptor clarity — customers should immediately recognize your business name on their statement

- Remove ambiguous or compliance-sensitive language — any product claims that imply medical outcomes

- Verify product descriptions are consistent — across homepage, product pages, checkout, and FAQs

- Make support contact highly visible — email, phone, or chat should be easy to find from any page

If your site contributed to dispute escalation or underwriting concerns, fix it now — before a new provider reviews it.

For a complete website compliance checklist: Peptide Merchant Account Requirements.

For a guide on building a compliant peptide website: Compliant Peptide Website for Payment Processing.

Step 4: Analyze Your Chargeback History

Chargebacks are the most common termination driver. Before reapplying, you need to understand your dispute patterns.

Ask yourself:

- Did disputes spike recently? What triggered the increase?

- Were shipping delays increasing around the same time?

- Did fraud attempts rise without adequate filters catching them?

- Did approval rates suddenly change before termination?

- Were customers confused about products, billing, or policies?

If dispute control was weak, strengthen it before reapplying. A new processor will review your history — showing you've identified and addressed the root cause is critical.

For a detailed guide on dispute prevention: How to Reduce Chargebacks in a Peptide Ecommerce Store.

If you need tools to prevent disputes proactively: Chargeback Protection.

Step 5: Review Your Reserve Situation

If your account had a rolling reserve, those funds may still be held temporarily after termination. Don't assume funds are permanently lost — reserve timelines typically follow chargeback windows (90–180 days).

Key things to know:

- Reserves are held to cover potential future chargebacks — not as a penalty

- The release timeline should be documented in your original merchant agreement

- You may need to request a final accounting from your previous processor

- Disputes filed after termination can be deducted from held reserves

Understand how reserve structures work: Rolling Reserves Explained for Peptide Merchant Accounts.

Step 6: Do Not Apply Randomly to Multiple Processors

This is one of the most common and costly mistakes after termination.

Submitting multiple applications rapidly can:

- Trigger additional scrutiny — processors share information and patterns are visible

- Raise red flags during underwriting — multiple recent declines signal instability

- Complicate MATCH situations — repeated applications make your profile look worse

- Lead to additional declines — each rejection makes the next one harder

Instead, take a targeted approach. Apply through a structured high-risk pathway with a provider who understands peptide businesses and has banking relationships that accommodate your category.

Learn about properly structured setups: High-Risk Merchant Accounts.

Step 7: Apply Through a Peptide-Friendly Underwriting Program

The most stable recovery path includes:

- Transparent volume expectations — be accurate about what you process monthly

- Accurate ticket size disclosure — don't understate your average order value

- Documented fraud control improvements — show what you've added since termination

- Clear fulfillment structure — shipping timelines, tracking, and customer support processes

- Proper category underwriting — with a bank that knows how to evaluate peptide businesses

Peptide businesses benefit from category-aligned approvals that set realistic thresholds and expectations from day one.

Consider LegitScript certification as part of your recovery. LegitScript certification independently verifies your compliance and dramatically improves approval odds with acquiring banks. Unison is a LegitScript partner and offers discounted certification — getting certified before reapplying makes your application significantly stronger.

See peptide-specific underwriting options: Peptides & Research Chemicals.

For a step-by-step approval preparation guide: How to Get Approved for a Peptide Merchant Account.

Step 8: Consider Diversifying Payment Methods

When rebuilding your payment setup, don't rely solely on card processing. Adding alternative payment rails can reduce your overall risk exposure and provide a backup if one channel faces issues.

- **ACH processing** works well for repeat buyers and larger orders — lower dispute dynamics than cards

- Multiple merchant accounts (when properly disclosed) can spread volume risk across banks

Explore ACH as part of a balanced acceptance strategy: ACH Payment Processing.

Warning Signs to Avoid Re-Termination

When you resume processing, monitor these metrics closely — especially in the first 90 days:

- Dispute ratio trends — catch increases early, before they breach thresholds

- Fraud attempt patterns — spikes may indicate card-testing attacks

- Shipping delay frequency — delays correlate with "item not received" disputes

- Decline rate changes — could signal your processor tightening risk controls

- Volume spikes — communicate planned growth to your account manager proactively

If instability appears early, correct it immediately. Termination recovery is about building predictability — proving to your new bank that your risk is controlled and manageable.

If you're seeing early warning signs: Why Peptide Payments Keep Getting Declined.

How Long Does Recovery Take?

Recovery timelines vary depending on:

- Whether MATCH is involved — MATCH adds complexity and documentation requirements

- Your prior dispute history — clean recent history is stronger than explanations

- Documentation readiness — formation docs, bank statements, processing history, and a clear narrative

- Website compliance improvements — demonstrating you've fixed what went wrong

- Volume and ticket profile — realistic expectations aligned with your actual business

Well-prepared applications through a high-risk specialist can move in days to weeks. Rushed, unprepared applications through random providers can stall for months — or fail entirely.

The Goal: Long-Term Stability, Not Just Fast Approval

When recovering from termination, your objective should be:

- Sustainable approvals with a bank that understands your category

- Controlled dispute ratios well below network thresholds

- Predictable funding without surprise holds or delays

- Reduced reserve pressure that improves over time with strong performance

- Scalable infrastructure that supports growth without triggering risk brakes

Rushing back into unstable processing increases the risk of repeat termination — and a second termination is significantly harder to recover from than the first.

If you need help stabilizing and rebuilding: Contact Unison.