You have decided that an ATM makes sense for your business. The next question is how you get one. Do you buy it, lease it, or take a free placement deal?

Each option has trade-offs, and the right choice depends on your budget, how involved you want to be, and how much risk you are comfortable with. This guide breaks down the real numbers — not the sales pitch — so you can make the decision that puts the most money in your pocket.

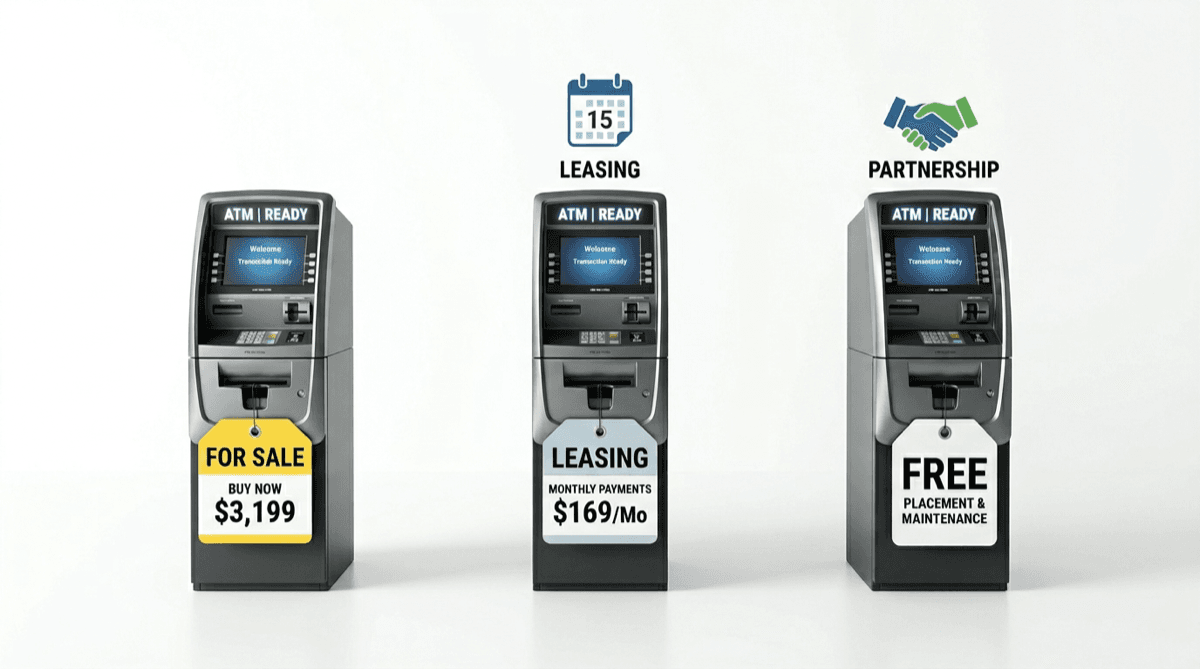

The Three Options at a Glance

| **Buy** | **Lease** | **Free Placement** | |

|---|---|---|---|

| **Upfront cost** | $2,500–$5,000 | $50–$150 first month | $0 |

| **Monthly cost** | $0 (you own it) | $50–$150/month | $0 |

| **Revenue per transaction** | 100% of surcharge | 100% of surcharge minus lease | Revenue share ($0.50–$1.00) |

| **Cash loading** | You handle or pay $100–$300/mo | You handle or pay $100–$300/mo | Included free |

| **Maintenance** | Your responsibility | Varies by lease | Included free |

| **Compliance** | Your responsibility | Varies by lease | Included free |

| **Risk** | You bear all risk | Shared | Provider bears all risk |

| **Best for** | High-traffic locations, hands-on owners | Testing before buying | Everyone else |

Option 1: Buying an ATM — Maximum Revenue, Maximum Responsibility

When you buy an ATM, you own the hardware outright and keep 100% of the surcharge revenue. At a $3.00 surcharge and 300 transactions per month, that is $900/month gross revenue.

The real costs most sellers downplay:

- Machine purchase: $2,500–$5,000 for a new, EMV-compliant ATM (Genmega, Hyosung, Triton are common brands)

- Processing account setup: $0–$200 one-time

- Initial cash float: $2,000–$5,000 (this is YOUR money sitting inside the machine)

- Cash loading: Either you drive to the bank, withdraw cash, and load it yourself (free but time-consuming) or you hire an armored car service ($100–$300/month)

- Maintenance and repairs: Paper rolls ($10/month), occasional part replacements ($50–$200), annual network certification. Budget $50–$150/month on average.

- Internet connectivity: $30–$75/month for a dedicated phone line or cellular connection

- Processing fees: $0.20–$0.50 per transaction

Real net income calculation (buying):

- Gross revenue: $900/month (300 transactions × $3.00)

- Processing fees: -$120 (300 × $0.40)

- Cash loading (armored): -$150/month

- Maintenance average: -$75/month

- Internet: -$50/month

- Net income: ~$505/month

If you load cash yourself, you save $150/month but spend 2–4 hours per week doing it.

Payback period: At $505/month net, a $3,500 machine pays for itself in approximately 7 months (excluding the cash float, which is always yours).

Pros: Highest per-transaction revenue. Full control. No revenue sharing. Asset ownership.

Cons: Capital investment. Operational responsibility. You handle maintenance, cash loading, compliance, and troubleshooting. If the machine breaks, you pay to fix it.

Option 2: Leasing an ATM — Lower Entry, Ongoing Payments

Leasing reduces the upfront cost while giving you most of the ownership benefits during the lease term. Typical leases run 12–36 months at $50–$150/month.

Cost breakdown:

- First month payment: $50–$150

- Monthly lease: $50–$150 for the term

- Everything else: Same as buying (cash loading, maintenance, internet, processing)

Real net income calculation (leasing at $100/month):

- Gross revenue: $900/month

- Processing fees: -$120

- Cash loading: -$150

- Maintenance: -$75

- Internet: -$50

- Lease payment: -$100

- Net income: ~$405/month

At the end of the lease, you typically have a buyout option ($1 to several hundred dollars) to own the machine.

Pros: Lower upfront cost. Same revenue as buying during the term. Buyout option.

Cons: Lower net income than buying. Still responsible for cash loading, maintenance, and compliance. Total cost over a 36-month lease often exceeds the purchase price.

Option 3: Free ATM Placement — Zero Cost, Zero Effort

A placement provider — like Unison Payment Solutions — installs an ATM in your business at no cost. They handle everything. You earn a share of each surcharge.

Cost breakdown:

- Everything: $0

What the provider handles: Machine, installation, cash loading, maintenance, repairs, monitoring, compliance, processing, signage.

What you provide: Floor space and electricity.

Real income calculation (free placement at $0.75/transaction):

- Revenue share: $225/month (300 transactions × $0.75)

- Your costs: $0

- Net income: $225/month

Your per-transaction income is lower than buying ($0.75 vs. ~$1.68 net). But your total cost is $0, your time investment is zero, and your risk is zero. You earn $225/month from doing literally nothing.

Pros: Zero investment. Zero effort. Zero risk. Income starts immediately. No maintenance, cash loading, or compliance responsibilities.

Cons: Lower per-transaction revenue. You share the surcharge with the provider. No asset ownership.

Which Option Makes You the Most Money?

If your location processes 500+ transactions/month and you have $5,000+ to invest and the time to manage operations, buying generates the highest long-term return. You will net $700–$1,500/month and recoup your investment within 4–6 months.

If you want to test the waters before committing capital, a 12-month lease lets you validate transaction volume at your location. If the numbers work, buy the machine at lease-end.

If you want passive income with zero risk — which is most business owners — free placement is the clear winner. You will earn less per transaction, but you will earn it from day one with no capital at risk, no time spent, and no operational burden. If you factor in the value of your time (loading cash, troubleshooting, dealing with maintenance), free placement often produces a higher effective hourly return than buying.

Our recommendation: Start with free placement. See how many transactions your location actually generates over 3–6 months. If volume exceeds 400/month and you want to maximize revenue, consider buying your own machine with the data to prove the investment is worth it. If volume is moderate (150–350/month), free placement is almost always the better financial decision because the operational costs of owning eat into the margins.

Red Flags to Watch For

Regardless of which option you choose, avoid providers who:

- Lock you into long-term contracts (3+ years) with early termination fees

- Charge "monthly service fees" on top of lease payments

- Will not disclose the surcharge split clearly

- Require you to use their processing exclusively (preventing you from shopping rates)

- Charge for maintenance or repairs that should be included

Unison Payment Solutions offers month-to-month terms, transparent revenue sharing, and full-service management with no hidden fees. We recommend starting with free placement, but we support all three models.

Get a free ATM for your business → or call (925) 290-6003 for a no-obligation consultation.