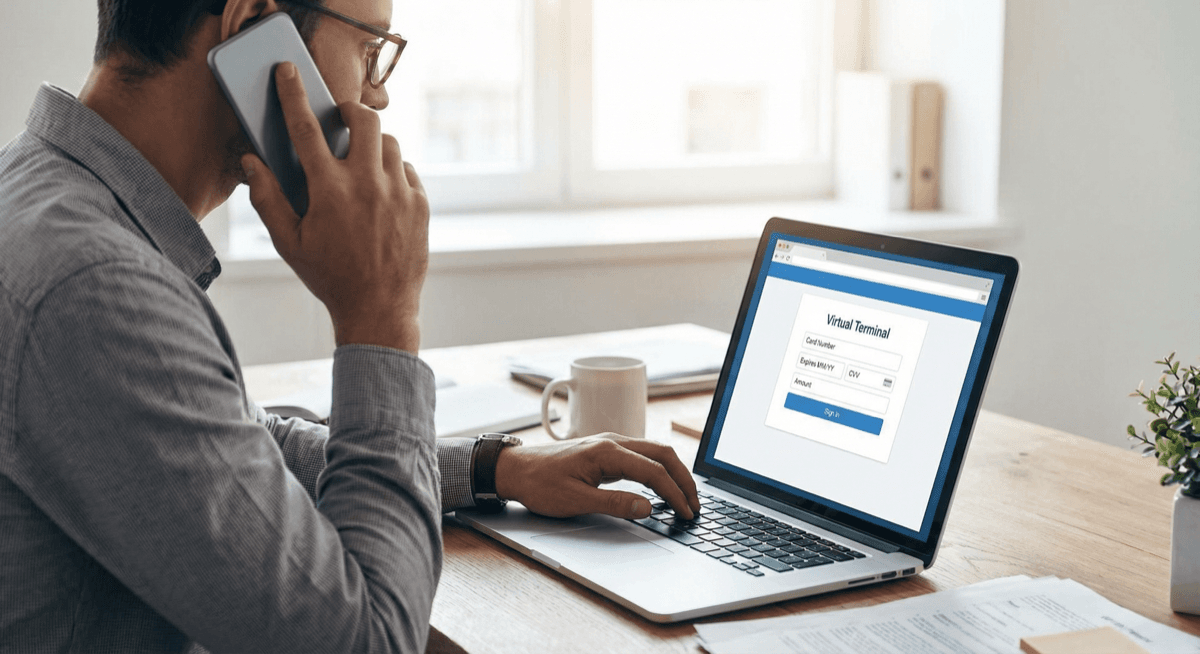

A virtual terminal is a web-based application that lets you process credit card payments from any computer or mobile device with internet access. Instead of swiping or tapping a physical card, you manually enter the card number, expiration date, and CVV into a secure online form. Virtual terminals are used for phone orders, mail orders, invoices, and any situation where the cardholder isn't physically present.

How Virtual Terminal Processing Works

1. Customer provides card details — by phone, email, fax, or mail order form 2. You log into the virtual terminal — a secure web portal accessible from any browser 3. Enter the payment information — card number, expiration, CVV, billing address, and amount 4. Submit for authorization — the payment gateway routes the transaction through the card networks 5. Receive instant approval or decline — funds are deposited to your bank account within 1-2 business days

No hardware. No app downloads. No card reader. Just a computer and an internet connection.

Who Uses Virtual Terminals?

Virtual terminals are essential for businesses that take payments when the customer isn't standing in front of them:

- Service businesses — contractors, consultants, agencies billing by phone or email

- B2B companies — processing purchase orders and invoice payments

- Mail order businesses — receiving orders by mail or fax

- Professional services — law firms, medical offices, accountants collecting payments remotely

- Non-profits — processing donations over the phone

- Any business taking phone orders — restaurants with delivery, appointment-based services

Virtual Terminal vs Physical Terminal vs Payment Gateway

| Feature | Virtual Terminal | Physical Terminal | Payment Gateway |

|---|---|---|---|

| Hardware required | No — browser only | Yes — card reader | No — API integration |

| Card present | No — key-entered | Yes — chip/tap/swipe | No — online checkout |

| Best for | Phone/mail/invoice | In-person retail | eCommerce websites |

| Processing rates | Higher (CNP rates) | Lower (CP rates) | Higher (CNP rates) |

| Setup time | Minutes | 1-3 days (shipping) | Days-weeks (development) |

Virtual Terminal Use Cases by Industry

| Industry | Primary Use | Typical Transaction |

|---|---|---|

| Contractors / Trades | Collect payment after job completion by phone | $500-5,000 |

| Law firms | Retainer deposits and fee collection | $1,000-10,000+ |

| Medical / Dental offices | Patient co-pays and balances by phone | $50-500 |

| B2B / Wholesale | Invoice payments from corporate clients | $1,000-50,000+ |

| Non-profits | Phone donations and pledge collections | $25-500 |

| Property management | Rent and maintenance fee collection | $500-3,000 |

| Consulting / Agencies | Monthly retainer billing | $1,000-10,000 |

| Government | Permit fees, fines, and service charges | $25-1,000 |

For B2B companies, virtual terminals are especially valuable because they support Level 2/3 data entry — capturing PO numbers, tax amounts, and line-item details that qualify corporate card transactions for lower interchange rates.

Virtual Terminal Security

Since virtual terminals process card-not-present (CNP) transactions, security is critical. Here's how legitimate virtual terminals protect your business:

PCI DSS compliance. Your virtual terminal provider must be PCI-compliant. PayTrace (Unison's gateway) is Level 1 PCI DSS certified — the highest certification level, audited annually by a Qualified Security Assessor.

Tokenization. After the first transaction, the virtual terminal stores a token (not the actual card number) for future charges. You never see or store raw card data on your computer.

TLS encryption. All data transmitted between your browser and the virtual terminal server is encrypted. Card details cannot be intercepted in transit.

AVS (Address Verification). The system checks the billing address against the card issuer's records. Mismatches flag potential fraud.

CVV verification. Requiring the 3-digit CVV code confirms the customer has the physical card (or at least the CVV), reducing fraud risk on phone orders.

Key Features to Look For

Recurring billing lets you set up scheduled payments — monthly retainers, subscription fees, installment plans. The system charges the stored card automatically on your schedule. You set the amount, frequency (weekly, monthly, quarterly), start date, and end date. Failed charges trigger automatic retry and notification.

Invoicing lets you email professional invoices with a "Pay Now" button. The customer clicks, enters their card on a secure hosted page, and the payment processes automatically. No phone call needed. Reduces your collections effort from days to minutes.

Tokenization securely stores card information so returning customers can be charged without re-entering their full card number. Essential for recurring billing and repeat customers. Reduces PCI scope because you never store raw card data.

Multi-user access lets multiple employees process payments from different computers with individual logins and permission levels. Track who processed what and when. Restrict refund capabilities to managers only.

Reporting and exports give you transaction history, batch summaries, and exportable data for accounting and reconciliation. QuickBooks and Xero integrations sync payments automatically.

Virtual Terminal Processing Rates

Virtual terminal transactions are classified as "card-not-present" (CNP), which carries higher interchange rates than in-person transactions because of increased fraud risk:

| Transaction Type | Typical Rate (Interchange-Plus) |

|---|---|

| Card-present (chip/tap) | 1.5-2.5% + $0.05-0.15 |

| Card-not-present (virtual terminal) | 2.0-3.0% + $0.10-0.20 |

| Keyed with AVS + CVV | Lower end of CNP range |

| Keyed without AVS/CVV | Higher end of CNP range |

Pro tip: Always enter the billing ZIP code and CVV when processing virtual terminal transactions. This qualifies you for lower CNP interchange tiers and reduces fraud disputes.

Unison's Virtual Terminal: PayTrace

Unison Payment provides virtual terminal access through PayTrace — a Level 1 PCI-compliant payment gateway that includes:

- Virtual terminal for manual card entry

- Recurring billing and subscription management

- Email invoicing with hosted payment pages

- Customer vault for secure card storage

- Detailed reporting and batch management

- Multi-user access with role-based permissions

- ACH/eCheck processing alongside card payments

PayTrace integrates with QuickBooks, Xero, and major accounting platforms. If you already use a virtual terminal elsewhere, Unison can migrate your stored customer data.

Need a virtual terminal? Contact Unison for a free PayTrace setup →

Related resources:

- PayTrace Gateway — our virtual terminal and gateway solution

- Invoicing & Surcharging — send invoices with payment links

- ACH Payment Processing — add bank transfer payments